Roth IRA vs. 401k: Which Should You Choose First?

If you’ve been following this series, you now know what a Roth IRA is, how to open one, and how to invest inside it. But at some point, especially if you have a job that offers a 401k, you’re going to ask yourself: should I invest in a Roth IRA or 401k first?

It’s one of the most common personal finance questions, and the honest answer is: it depends. But “it depends” is only useful if you have a clear framework for deciding. That’s what this post gives you.

Roth IRA vs 401k: A Simple Starting Strategy

If you’re deciding between a Roth IRA and a 401k:

- Contribute to your 401k up to the employer match first (free money)

- Then prioritize a Roth IRA for tax-free growth

- Then return to your 401k for additional contributions

First: What Is a 401k?

Before comparing the two, a quick primer on 401ks for those who are new to the term.

A 401k is a retirement savings account offered through your employer. Unlike a Roth IRA, which you open yourself, a 401k is set up through your workplace. Contributions come directly out of your paycheck before you ever see the money.

Here’s how it works:

- You choose a percentage of your paycheck to contribute

- That money goes into your 401k before taxes are taken out – meaning you pay less in income taxes today

- Your money grows tax-deferred – you don’t pay taxes on it until you withdraw in retirement

- Many employers match a portion of what you contribute – meaning free money added to your account

The 2026 contribution limit for a 401k is $24,500 (or $32,500 if you’re 50 or older) — significantly higher than the Roth IRA limit of $7,500.

How They’re Different

| Roth IRA | 401k | |

|---|---|---|

| Who opens it | You | Your employer |

| Contribution limit (2026) | $7,500 | $24,500 |

| Tax treatment | After-tax contributions, tax-free withdrawals | Pre-tax contributions, taxed when withdrawn |

| Employer match | No | Often yes |

| Investment options | Wide – you choose | Limited to what your employer offers |

| Income limits | Yes | No |

| Early withdrawal | Contributions accessible anytime | Penalties before age 59½ |

| Roth version available | Yes (Roth IRA) | Yes (Roth 401k, if your employer offers it) |

You may also notice your employer’s 401k plan offers a Roth 401k option. Like a Roth IRA, contributions are after-tax and withdrawals in retirement are tax-free – but it follows 401k contribution limits, not Roth IRA limits. It’s worth knowing it exists, and we’ll cover it in a dedicated post. One thing to note: Roth IRAs have income limits that determine who can contribute – if you haven’t already, check our What Is a Roth IRA post → for the full breakdown.

The Key Difference: When You Pay Taxes

This is the most important thing to understand about both accounts.

With a 401k, you contribute pre-tax money – meaning you get a tax break today, but you’ll pay income taxes on everything you withdraw in retirement.

With a Roth IRA, you contribute money you’ve already paid taxes on – meaning no tax break today, but your withdrawals in retirement are completely tax-free.

Which is better? It comes down to one question: do you expect to be in a higher or lower tax bracket in retirement than you are now?

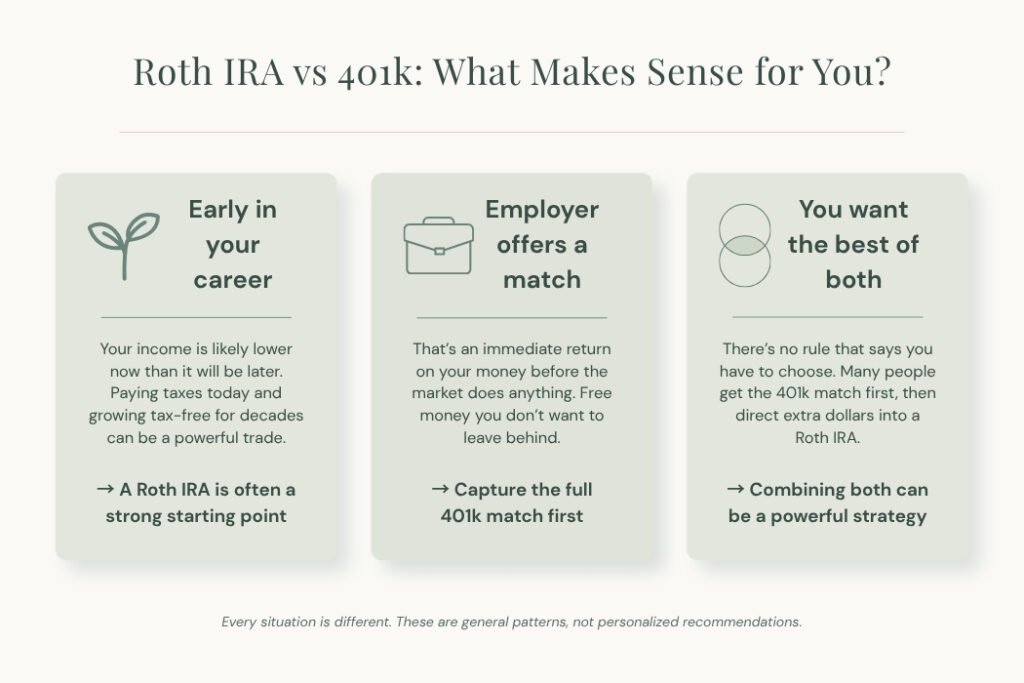

- If you expect to earn more later (likely if you’re early in your career), paying taxes now at a lower rate and having tax-free withdrawals later makes the Roth IRA more advantageous.

- If you expect your income to be lower in retirement, deferring taxes now with a 401k could save you more in the long run.

For most people who are earlier in their careers and expect their income to grow, the Roth IRA tends to win on the tax math. But this isn’t universal – everyone’s situation is different, and a tax professional can give you guidance specific to your circumstances.

This content is for educational purposes only and not financial advice. Always consult a licensed financial or tax professional for guidance specific to your situation.

The Employer Match – Don’t Leave Free Money on the Table

If your employer offers a 401k match, that changes the equation significantly.

A 401k match is when your employer contributes money to your 401k based on what you contribute – for example, matching 50% of your contributions up to 6% of your salary. That’s an immediate 50% return on part of your investment before the market does anything.

The general principle: if your employer offers a match, contributing enough to capture the full match is almost always worth doing before directing additional dollars elsewhere, including into a Roth IRA.

We’ll go deeper on how employer matches work, how to calculate yours, and how to make the most of them in a dedicated 401k post. For now, the key takeaway is: if a match is on the table, don’t ignore it.

Roth IRA vs 401k: Which One Fits Your Situation?

If you’re wondering whether a Roth IRA or 401k is better for you, the answer depends on your situation. Here’s a simple way to think about it before deciding what to prioritize first.

A Simple Framework for Deciding

Rather than declaring one account universally better, here’s a simple way to decide which one makes the most sense for your own situation:

Step 1: Does your employer offer a 401k match? If yes: contribute enough to your 401k to capture the full match first. This is free money. If no: skip to Step 2.

Step 2: Open and contribute to a Roth IRA Up to the 2026 limit of $7,500/year. This is your highest-priority account for tax-free long-term growth, especially if you’re earlier in your career.

Step 3: Do you have more to invest after maxing your Roth IRA? Go back to your 401k and contribute more, up to the $24,500 limit.

Step 4: Still more to invest? Consider a taxable brokerage account for additional flexibility.

This order isn’t a rule; it’s a framework. Your specific tax situation, income, employer benefits, and goals all matter. But for most people who are building from scratch, this sequence makes sense.

What If You Don’t Have a 401k?

Not everyone has access to a 401k, especially if you’re self-employed, work part-time, or work for a small employer that doesn’t offer one.

If that’s your situation, the Roth IRA becomes even more important. It’s the primary tax-advantaged retirement account available to you, and prioritizing it is straightforward.

There are also retirement accounts designed specifically for self-employed people, like a SEP-IRA or Solo 401k, that offer higher contribution limits. We’ll cover those in a future post.

Can You Have Both?

Yes, and many people do. There’s no rule that says you have to choose one or the other. You can contribute to both a 401k and a Roth IRA in the same year, as long as you stay within the limits for each.

Having both actually gives you flexibility in retirement: you’ll have a mix of pre-tax money (401k) and tax-free money (Roth IRA) to draw from, which can be a powerful tool for managing your tax burden later in life.

FAQs: Roth IRA vs 401k

Can you contribute to both a Roth IRA and 401k?

Yes, you can contribute to both in the same year as long as you stay within each account’s limits.

Is a Roth IRA better than a 401k?

Neither is universally better. A Roth IRA offers tax-free withdrawals, while a 401k offers upfront tax savings and potential employer matching.

Should beginners choose a Roth IRA or 401k?

If your employer offers a match, start with the 401k. Otherwise, many beginners benefit from starting with a Roth IRA.

The Bottom Line

Neither account is universally better – they serve different purposes and offer different advantages. But here’s a simple way to think about it:

- Start with your 401k if your employer matches – capture that free money first

- Then prioritize your Roth IRA, especially if you’re early in your career and expect your income to grow

- Come back to your 401k if you have more to invest after maxing your Roth IRA

The best move is the one you can sustain consistently. Whether that’s $25 a month into a Roth IRA, enough to get your employer match in a 401k, or both, starting is always better than waiting. Because building wealth isn’t about perfection, it’s about consistency.

This Wraps Up the Roth IRA Series

This post is the final one in our Roth IRA series. Here’s the full arc, in order:

- 👉 How to Start Investing With Little Money →

- 👉 What Is a Roth IRA? →

- 👉 How to Open a Roth IRA at Fidelity →

- 👉 How to Invest Inside Your Roth IRA — Starting With $5 →

- 👉 Roth IRA vs. 401k – Which One Should You Choose First? (You are here)

Coming next:

- 👉 Best Index Funds for Beginners → (Coming soon)

- 👉 Grab the free Credit Clarity Checklist →