What Is a Roth IRA – How It Works and Why It’s One of the Most Powerful Investing Accounts

If you’ve ever Googled “what is a Roth IRA” or “how to start investing,” you’ve probably seen the term Roth IRA come up over and over. And if no one ever explained what it actually means, it’s easy to keep scrolling past it.

This post is a full breakdown – what a Roth IRA is, how it works, and why it’s worth understanding before you invest a single dollar.

What Is a Roth IRA?

A Roth IRA is an individual retirement account that lets your money grow completely tax-free. Let’s break that down:

- Individual — it’s yours personally, not tied to an employer. You open it yourself, you control it, and it follows you no matter where you work.

- Retirement account — it’s designed for long-term investing, typically money you plan to leave untouched until age 59½ or older.

- Tax-free growth — this is what makes it different from almost every other investment account, and we’ll get into the details below.

You can open a Roth IRA at a brokerage like Fidelity, Schwab, or Vanguard with $0. Once it’s open, you contribute money and invest it – in index funds, ETFs, or other investments of your choice. Your money then grows over time, and when you eventually withdraw it in retirement, you pay zero taxes on any of it.

How Roth IRA Tax-Free Growth Works

The key is understanding the difference between taxed growth and tax-free growth – because that’s where the real power of this account lives.

In a regular taxable investment account, some of your growth may be reduced by taxes on dividends or capital gains over time. In a Roth IRA, qualified withdrawals in retirement are completely tax-free.

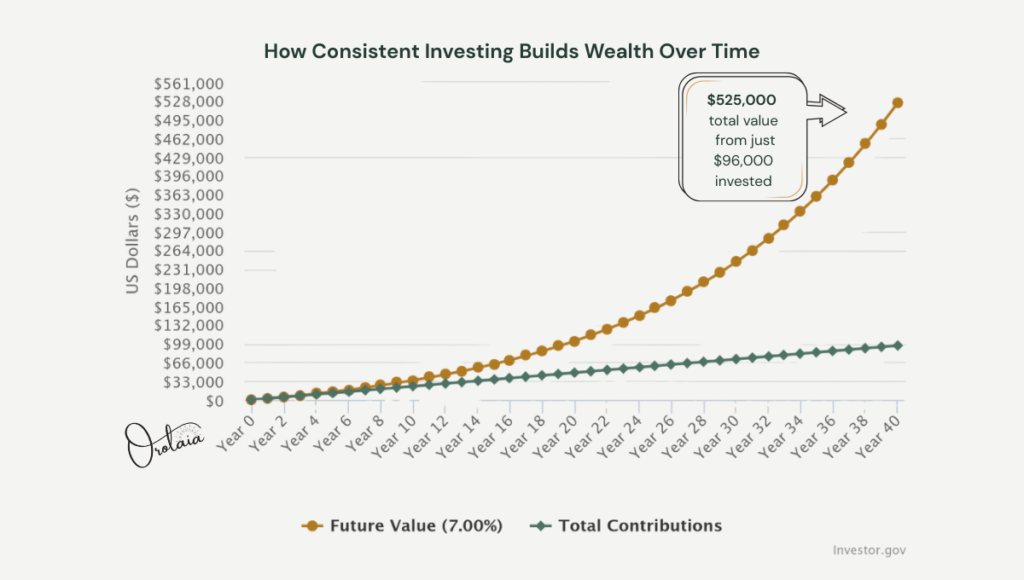

Here’s what that looks like in real numbers:

Imagine you invest $200 a month starting today. At an average annual return of 7%, over 40 years you’d have approximately $525,000.

In a regular taxable account, some of that growth could be reduced by taxes along the way. In a Roth IRA, those investments grow without annual taxes – and qualified withdrawals in retirement are tax-free.

In other words, that entire $525,000 could be yours to keep.

The longer your money stays invested, the more powerful that tax-free compounding becomes. That’s not unique to any one type of investor – it’s just how the math works.

This content is for educational purposes only and not financial advice. Actual returns will vary based on market performance and individual circumstances.

Roth IRA Contribution Limits (2026)

The IRS sets annual limits on how much you can put into a Roth IRA each year.

2026 contribution limits:

- Under age 50: $7,500/year — about $625/month or $144/week

- 50 or older: $8,600/year (includes a catch-up contribution of $1,100)

A few important rules:

- You can contribute up to the limit – you don’t have to hit it. Even $25 a month counts.

- You can contribute to a Roth IRA and a workplace 401(k) in the same year – they have separate limits.

- You have until Tax Day (typically April 15) to make contributions for the prior tax year. So in April 2027, you can still make 2026 contributions.

- You can only contribute earned income – meaning money from a job, freelance work, or self-employment. Investment income doesn’t count.

Roth IRA Income Limits

Not everyone can contribute to a Roth IRA – the IRS phases out eligibility at higher income levels.

The limits below apply to the 2026 tax year.

| Filing Status | Full Contribution | Partial Contribution | No Contribution |

| Single / Head of Household | Under $153,000 | $153,000–$168,000 | Over $168,000 |

| Married Filing Jointly | Under $242,000 | $242,000–$252,000 | Over $252,000 |

If your income is in the “partial” range, you can still contribute – just a reduced amount. If you’re over the limit entirely, there are other strategies available (like a backdoor Roth IRA), but that’s a topic for a more advanced post.

For most people who are earlier in their careers or building their financial foundation: you very likely qualify for the full contribution.

Roth IRA vs Traditional IRA: What’s the Difference?

You may have also heard of a Traditional IRA. Here’s how they compare:

| Roth IRA | Traditional IRA | |

| When you pay taxes | Now (contributions are after-tax) | Later (pay taxes when you withdraw) |

| Growth | Tax-free | Tax-deferred |

| Withdrawals in retirement | Tax-free | Taxed as income |

| Required withdrawals | None | Must start at age 73 |

| Best for | Those who expect to be in a higher tax bracket later | Those who expect to be in a lower tax bracket later |

For most people who are earlier in their earning years – and expect their income to grow over time – the Roth IRA tends to be the stronger choice. Paying taxes on contributions now, and never paying again on decades of growth, is generally the better trade.

Can You Withdraw Money from a Roth IRA?

Here’s something most people don’t know about Roth IRAs: you can withdraw your contributions (not your earnings) at any time, for any reason, penalty-free (more info from Fidelity here).

That means if you contribute $5,000 this year and face a genuine emergency two years from now, you can take that $5,000 back out without penalty. The earnings stay invested, but your original contributions are always accessible.

This makes the Roth IRA particularly well-suited for anyone still building their financial foundation. It’s not a locked vault. It’s a long-term investment account that also gives you a degree of flexibility when life doesn’t go according to plan.

Why a Roth IRA Is So Powerful for Long-Term Investing

Most of our parents worked hard and saved what they could. But long-term, tax-free investing wasn’t something many of them had access to – or that anyone explained to them. The Roth IRA has existed since 1997, and it’s available to anyone with earned income, starting with their very first dollar.

Wherever you are in your financial journey, the best time to open one is as soon as you’re eligible. Every year your money grows tax-free inside a Roth IRA is a year working in your favor. Starting now, with whatever amount is realistic for you, will always be better than waiting for the “right” moment or the “right” amount.

That’s not motivation. That’s just math.

And the wealth built this way – steadily, tax-free, over years – doesn’t just change your own future. It changes what you’re able to pass on.

Quick Recap:

Roth IRA Benefits

- ✅ Your money grows completely tax-free

- ✅ No taxes when you withdraw in retirement

- ✅ You control it — not your employer

- ✅ Start with $0 — no minimum to open

- ✅ Contribute as little as $5 at a time

- ✅ Your contributions are always accessible in an emergency

- ✅ 2026 limit: $7,500/year (under 50) / $8,600/year (50 and older)

Roth IRA FAQs

What is a Roth IRA in simple terms?

A Roth IRA is a retirement investment account where your money grows tax-free and you pay no taxes when you withdraw it in retirement.

Can I withdraw money from a Roth IRA?

Yes. You can withdraw your contributions at any time without taxes or penalties, but earnings generally must stay invested until age 59½.

How much can you contribute to a Roth IRA?

In 2026, individuals under age 50 can contribute up to $7,500 per year, while those 50 or older can contribute $8,600.

Is a Roth IRA better than a traditional IRA?

It depends on your tax situation, but many younger investors prefer Roth IRAs because they allow tax-free growth and tax-free withdrawals in retirement.

Ready to Open Yours?

Now that you understand what a Roth IRA is and how it works, the next step is opening one.

In the next post, we walk through exactly how to open a Roth IRA at Fidelity – step by step, from creating your account to making your first contribution.

Next in this series:

- 👉 How to Open a Roth IRA at Fidelity: Step by Step → (Coming soon)

- 👉 How to Invest Inside Your Roth IRA: Starting With Just $5 → (Coming soon)

New here? Start from the beginning:

- 👉 How to Start Investing With Little Money →

- 👉 Grab the free Credit Clarity Checklist → before you invest